The 2026 1099-NEC threshold drops to $2,000 for cash rewards paid to US recipients, and EU VAT rules still vary by member state even after One Stop Shop. A merchant of record for referral payouts acts as the legal payer when those rewards clear, absorbing withholding, tax filing and recipient documentation that otherwise sit with your finance team. If you pay partners in more than three countries or you're crossing 50 monthly payouts, the MoR service fee usually costs less than the headcount to track nexus filings, hand-generate 1099s and match payouts in finance-owned spreadsheets.

- What merchant of record means for referral payouts

- How a merchant of record handles referral payout compliance

- What compliance risks MoR removes for SaaS referral programs

- Merchant of record vs payment facilitator for referral payouts

- When SaaS companies should use MoR for referral payouts

- Merchant of record vs manual bank transfer and in-house billing

- How to compare MoR providers for your referral program

TLDR:

- A payout MoR becomes the legal payer for referral rewards, handling tax liability, withholding, 1099-NEC/DAC7 filing and VAT across multiple jurisdictions.

- From 2026, US cash rewards over $2,000 trigger 1099-NEC filing; an MoR collects W9s and files on your behalf.

- Payment facilitators clear transactions but leave tax calculation, withholding and compliance documentation on your finance desk.

- Consider MoR at 50+ payouts monthly, 3+ countries, or $100K+ Referral ARR; the 5-6% fee typically beats in-house build cost inside year one.

- Cello acts as legal payer of record with pre-built Stripe/Chargebee webhooks, server-side attribution and fraud detection; VEED runs referrals at 90.4% lower CAC.

What merchant of record means for referral payouts

Most SaaS teams first meet "merchant of record" through product billing. Paddle, Lemon Squeezy, and similar providers act as the legal seller when customers buy a subscription, taking on sales tax, VAT, and chargebacks so you skip registering in every jurisdiction.

Referral payouts flip that direction. Money flows out to users, partners, and affiliates instead of in from customers. A payout MoR becomes the legal payer when rewards are issued, moving obligations onto a third party:

- Payment processing across currencies and rails (PayPal, Venmo, others)

- Tax liability and withholding on payouts

- Payout documentation, credit notes, and recipient records

- Local rules governing reward income

Same legal mechanism, opposite cash direction, separate compliance surface.

How a merchant of record handles referral payout compliance

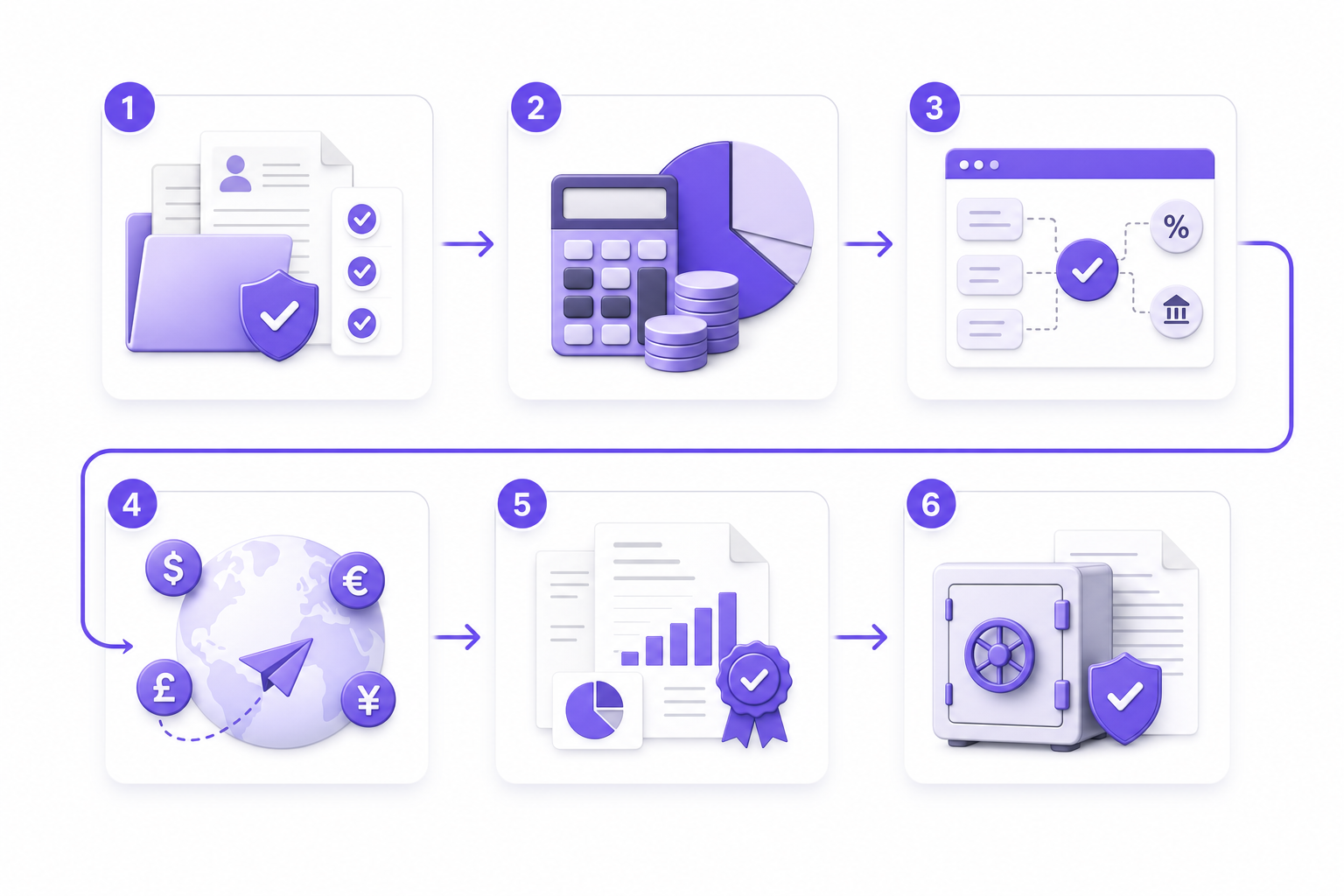

The lifecycle behind a single referral reward has six stages when an MoR sits in the flow:

- Partner enrollment with tax form collection. W9 for US-based referrers, W8-BEN for non-US individuals, W8-BEN-E for foreign entities, combined with identity verification including OFAC and EU consolidated list sanctions screening. No payout clears until the form is validated and the check passes.

- Earnings calculation tied to attributed conversions, with the MoR reading conversion events. Typically

invoice.paidorcharge.succeededwebhook signals from Stripe or Chargebee to calculate the reward against the campaign rules. The MoR books itself as the payer of record on the resulting credit note, keeping the SaaS company's accounts payable clean. - Withholding logic applied per jurisdiction, including treaty rates for cross-border partners. The US default rate on payments to non-resident referrers is 30%, reduced to the applicable treaty rate where one exists. For example, 15% for many EU residents under US-Germany or US-UK treaty provisions. The MoR holds the withheld amount and remits it to the IRS on the required schedule.

- Payout execution in 60+ supported currencies via local rails where available: SEPA credit transfer for EU recipients, ACH for US bank accounts, or PayPal globally. FX conversion is applied at disbursement, with the converted amount and exchange rate recorded against the payout record so recipients receive confirmation in their preferred currency.

- Year-end reporting (1099-NEC, DAC7, EU equivalents) generated and filed on behalf of the SaaS company. In the US, cash rewards crossing the $2,000 1099-NEC threshold in 2026 require a form filed with the IRS and delivered to the recipient by January 31 of the following year. In the EU, DAC7 requires reporting of referrer income to member-state tax authorities. Copies are available in the SaaS company's reporting dashboard.

- Audit trail retention covering every payout, tax form, and threshold check: the triggering conversion event, withholding calculation, exchange rate applied, and filing reference. Retention periods follow the longest applicable statutory requirement across jurisdictions: typically seven years for US federal tax records and ten years for EU VAT records.

What compliance risks MoR removes for SaaS referral programs

Structuring referral payouts through an MoR transfers four categories of exposure off your balance sheet:

- Cross-border indirect tax. The EU's €10,000 distance-selling threshold, the One Stop Shop scheme, and US state economic nexus rules stop being your registrations to track. The MoR holds the filings.

- US information reporting. From 2026, cash referral rewards above the $2,000 1099-NEC threshold require IRS filing. The MoR collects W9s and W8-BENs, generates forms, and files them.

- Data protection. GDPR and CCPA obligations over recipient PII sit with the MoR as controller or processor of payout data.

- AML and KYC. Sanctions screening, beneficial ownership checks, and threshold-driven due diligence scale with payout volume under the MoR's program.

The outcome: finance stops monitoring nexus across 50 states and 27 EU member states, legal stops drafting payout-specific DPAs per recipient, and auditors see one contractual counterparty instead of thousands of payee records.

Merchant of record vs payment facilitator for referral payouts

Payment facilitators and merchants of record both move money to referrers, but only one absorbs the compliance work. A PayFac (Stripe Connect, PayPal Payouts API) clears the transaction and stops there. Tax calculation, withholding, 1099 filing, and recipient documentation stay on your finance team's desk.

|

Dimension |

Merchant of record |

Payment facilitator |

|---|---|---|

|

Tax liability |

Held by MoR |

Retained by SaaS company |

|

Payout currencies |

60+ via local rails |

Often USD-first |

|

Compliance docs |

W9, W8-BEN, 1099-NEC, DAC7 |

You produce them |

|

Engineering effort |

Drop-in, MoR owns updates |

Ongoing regulation tracking |

|

Best use case |

Cross-border programs at scale |

Domestic, low-volume payouts |

Stripe Connect's per-payout fee looks low on a single transaction, but once you add headcount to track nexus, generate 1099s, and match payout records across jurisdictions, the total cost outpaces a flat MoR service fee well before you hit 50 monthly payouts.

When SaaS companies should use MoR for referral payouts

Five trigger signals tell you the MoR model has crossed into economic sense for your referral program:

- Payouts across more than three countries. Each new jurisdiction multiplies registration, withholding, and reporting work non-linearly.

- Rewards flowing to EU referrers or other high-VAT regions. VAT treatment of referral income varies by member state and gets harder to interpret as volume grows.

- More than 50 cash payouts a month. At that cadence, 1099 collection and threshold tracking stop being a quarterly task and require dedicated infrastructure.

- No dedicated finance or tax compliance headcount. One controller owning close, payroll, and audit prep means payout compliance will quietly slip.

- Referral ARR trending past $100K annually. Manual reconciliation against billing events breaks down well before that ceiling.

If two or more apply, the 5-6% service fee usually costs less than the headcount and risk of running payouts in-house.

Merchant of record vs manual bank transfer and in-house billing

Manual transfers and in-house billing look free on paper. The cost lives in places finance dashboards rarely surface.

|

Approach |

Hidden cost |

|---|---|

|

Manual bank transfer |

Collecting IBANs per recipient, initiating SEPA/ACH/wire batches, mapping payouts to tax jurisdictions, hand-generating 1099s and DAC7 returns, matching in finance-owned spreadsheets. |

|

In-house Stripe/PayPal build |

Engineering tickets for reward math, FX conversion, payout retries, audit logging, plus a new ticket every time a regulation changes in a market you operate in. |

|

MoR |

Flat fee, one counterparty, zero in-house tax engineering. |

An in-house build typically runs three to four sprints before it is production-ready, then carries a permanent maintenance tail as tax rules change across jurisdictions. The MoR fee usually clears the buy-versus-build threshold inside year one.

How to compare MoR providers for your referral program

Treat MoR procurement like any other infrastructure buy. Six questions separate genuine MoR providers from processors borrowing the label:

- Which payout rails and currencies are live today, not on a roadmap? PayPal global, Venmo US-only, local bank rails per country.

- Who signs the 1099-NEC and DAC7 filings, you or them?

- Is VAT remittance automated or invoice-only?

- What fraud controls ship by default: self-referral blocking, velocity checks, manual review queues?

- Pre-built webhooks for Stripe and Chargebee, or custom API work?

- Pricing tied to Referral ARR caps, or a percentage skim on every payout?

If a vendor hedges on tax filing ownership, they are a PayFac with better marketing.

What is a merchant of record for referral payouts?

The legal payer of record for rewards issued to users, partners, and affiliates. The MoR holds tax liability, files recipient documentation, and remits indirect taxes on the SaaS company's behalf.

Do I need to issue 1099s for referral rewards paid to users?

Yes, once cumulative cash rewards to a US recipient cross the $2,000 1099-NEC threshold in 2026. An MoR collects W9s at enrollment and files for you.

How does a referral program handle VAT on rewards paid in Europe?

Through the EU One Stop Shop scheme. The MoR calculates VAT per recipient country, remits to a single member-state authority, and issues matching credit notes.

MoR vs payment facilitator: what is the difference?

A PayFac moves money. An MoR moves money and absorbs tax, reporting, and recipient documentation liability.

Which countries require withholding tax on referral payments?

The US (non-resident recipients), Germany, France, Spain, Brazil, India, and most jurisdictions with treaty-based rules. The MoR applies the correct rate per recipient.

Does an MoR take over my payout approval workflow?

No. Campaign rules, eligibility logic, fraud review, and manual approval queues stay with you. The MoR takes over at disbursement and filing.

Can I use a merchant of record to handle payouts without changing my referral program's reward structure?

Yes. The MoR takes over payment processing, tax filing, and compliance documentation, but campaign rules, reward amounts, eligibility logic, and approval workflows remain under your control. You define what gets paid and to whom; the MoR handles how it's paid and reported.

What's the difference between an MoR and just using Stripe or PayPal for referral payouts?

Stripe and PayPal move money but leave tax liability, withholding, 1099 filing, and recipient documentation on your finance team. An MoR absorbs those obligations as the legal payer of record, collecting W9s and W8-BENs at enrollment and filing year-end forms on your behalf.

When should a SaaS company switch from manual bank transfers to an MoR for referral payouts?

When you're paying referrers across more than three countries, issuing more than 50 cash payouts monthly, or trending past $100K annual Referral ARR. At that scale, the 5-6% MoR platform fee costs less than the headcount and audit risk of in-house payout compliance.

How does an MoR handle referral rewards paid to partners who change countries mid-program?

The MoR tracks the recipient's registered tax residency at the time of each payout and applies the correct withholding rules and filing obligations for that jurisdiction. If a partner moves and updates their tax information, subsequent payouts follow the new country's rules. Year-end forms reflect the cumulative total per tax residency period.

Can we set different reward caps per referrer based on subscription tier or partner status?

Yes. Campaign-level configuration inside the MoR portal lets you define reward caps, eligibility rules, and payout structures per referrer segment. You can tie caps to subscription tier, partner classification, or any other attribute passed through your attribution system.

Do we need separate MoR agreements for user referrals and partner programs?

No. Most MoR providers unify user and partner payouts under one agreement with shared tax infrastructure, payout rails, and compliance workflows. The same 1099 filing, VAT remittance, and fraud detection logic applies to both motions, reducing administrative surface area.

MoR vs building a custom payout system: what breaks first at scale?

Tax rule changes, cross-border registration requirements, and recipient data management break first. A custom system requires engineering tickets every time a jurisdiction updates withholding logic, nexus thresholds, or filing deadlines. The MoR absorbs those updates across 60+ countries without your team tracking them.

How do we track referral payout ROI if the MoR sits between us and recipients?

The MoR provides real-time reporting dashboards showing total payouts, recipient count, and country-level breakdowns linked to your attribution system. You measure Referral ARR from your billing platform, subtract MoR fees and payout costs from the MoR's report, and calculate ROI the same way you would for any acquisition channel.

What happens to pending payouts if a referred customer refunds before the reward clears?

The MoR cancels the pending reward automatically when it receives the refund event from your billing system. If the payout already cleared, the MoR may issue a clawback request to the recipient or deduct the amount from their next eligible reward, depending on the program's terms.

Can we run referral payouts through an MoR without migrating our billing system?

Yes. The MoR integrates via webhooks or API with your existing Stripe, Chargebee, Paddle, or Recurly setup. Your billing system stays unchanged; the MoR receives conversion events and handles the payout and tax side independently.

How do MoR fees compare to the cost of hiring a compliance contractor for referral payouts?

A dedicated contractor typically costs $60K-$90K annually for a single region, plus legal review for cross-border work. The 5-6% MoR platform fee on Referral ARR usually breaks even at $100K-$150K annual payout volume, and scales across 60+ countries without additional headcount.

Best way to migrate from manual PayPal payouts to an MoR without losing historical data?

Export your historical payout records, recipient tax forms, and attribution mappings before go-live. The MoR imports active recipient profiles and continues forward-looking payouts from the cutover date. Historical 1099 and VAT filings for prior years remain your responsibility unless negotiated otherwise.

Can the MoR handle payouts in local currency even if our billing system invoices in USD?

Yes. The MoR converts from your invoiced currency to the recipient's preferred payout currency at the time of disbursement. You set the reward value in your base currency; the MoR applies real-time FX rates and handles local-rail transfers without you managing multi-currency accounting.